The United States is currently home to over 3,000 operational data centers, a number poised for significant expansion in the coming years. A comprehensive analysis by the Pew Research Center, drawing on data from Data Center Map, reveals that more than 1,500 new data centers are in various stages of development across the nation. This burgeoning growth signifies a critical juncture in the nation’s digital infrastructure, with a notable trend indicating a substantial migration of these vital facilities towards rural areas, a stark contrast to the urban concentration of existing centers. This shift has far-reaching implications for land use, economic development, and community engagement, prompting a deeper examination of the factors driving this transformation and the public’s evolving awareness and opinions regarding these essential, yet often unseen, technological hubs.

The Expanding Digital Footprint: Data Centers on the Rise

The proliferation of data centers is intrinsically linked to the exponential growth of digital information and the increasing demand for cloud computing, artificial intelligence, and other data-intensive technologies. These facilities, often sprawling complexes of servers and networking equipment, are the physical backbone of the internet and the digital economy. As of February 19, 2026, the Data Center Map database, a primary source for industry insights, identified over 3,000 active data centers across the U.S. This figure is not static; a further 1,500+ projects are classified as "under construction," "planned," or "land banked," indicating a robust pipeline of future development. This surge in construction underscores the ongoing investment and strategic importance placed on data infrastructure by technology giants and burgeoning enterprises alike.

The Pew Research Center’s analysis meticulously categorized and compiled data from Data Center Map, focusing on projects with clear development trajectories and excluding those marked as canceled or uncertain. This rigorous approach ensures a reliable snapshot of the current and future landscape of data center development in the United States. The research methodology also involved integrating U.S. Census Bureau classifications to understand the urban and rural distribution of these facilities, providing a crucial geographical context to this digital expansion.

A Ruralward Migration: The Changing Geography of Data Centers

A significant finding of the Pew Research Center’s analysis is the dramatic shift in the preferred locations for new data center construction. While the vast majority of currently operating data centers are situated in urban or suburban areas (87%), a striking 67% of planned data centers are slated for rural locations. This represents a substantial reversal of historical trends and signals a strategic recalibration in the industry’s site selection criteria.

Several factors are likely contributing to this ruralward migration. Firstly, the availability of land is a primary driver. Rural areas often offer larger tracts of undeveloped land at a lower cost compared to densely populated urban centers, accommodating the significant physical footprint of modern data centers. Secondly, the substantial energy requirements of these facilities necessitate access to reliable and often cost-effective power sources. Rural areas may offer access to cheaper electricity, particularly if located near power generation facilities or regions with abundant renewable energy potential. Furthermore, the increasing focus on environmental sustainability and the desire to minimize the visual and auditory impact on residential populations may also steer developers toward less populated regions. The availability of water for cooling systems, a critical operational component, can also be a consideration, with some rural areas offering more accessible and less contested water resources.

Regional Hotspots and State-Level Dominance

The planned expansion of data centers is not evenly distributed across the nation. The South and Midwest regions are emerging as the primary hubs for future development, collectively accounting for three-quarters of all planned data centers. The South alone is projected to host nearly half (48%) of these new facilities. This regional concentration is driven by a combination of favorable economic conditions, access to resources, and potentially state and local incentives aimed at attracting high-tech industries.

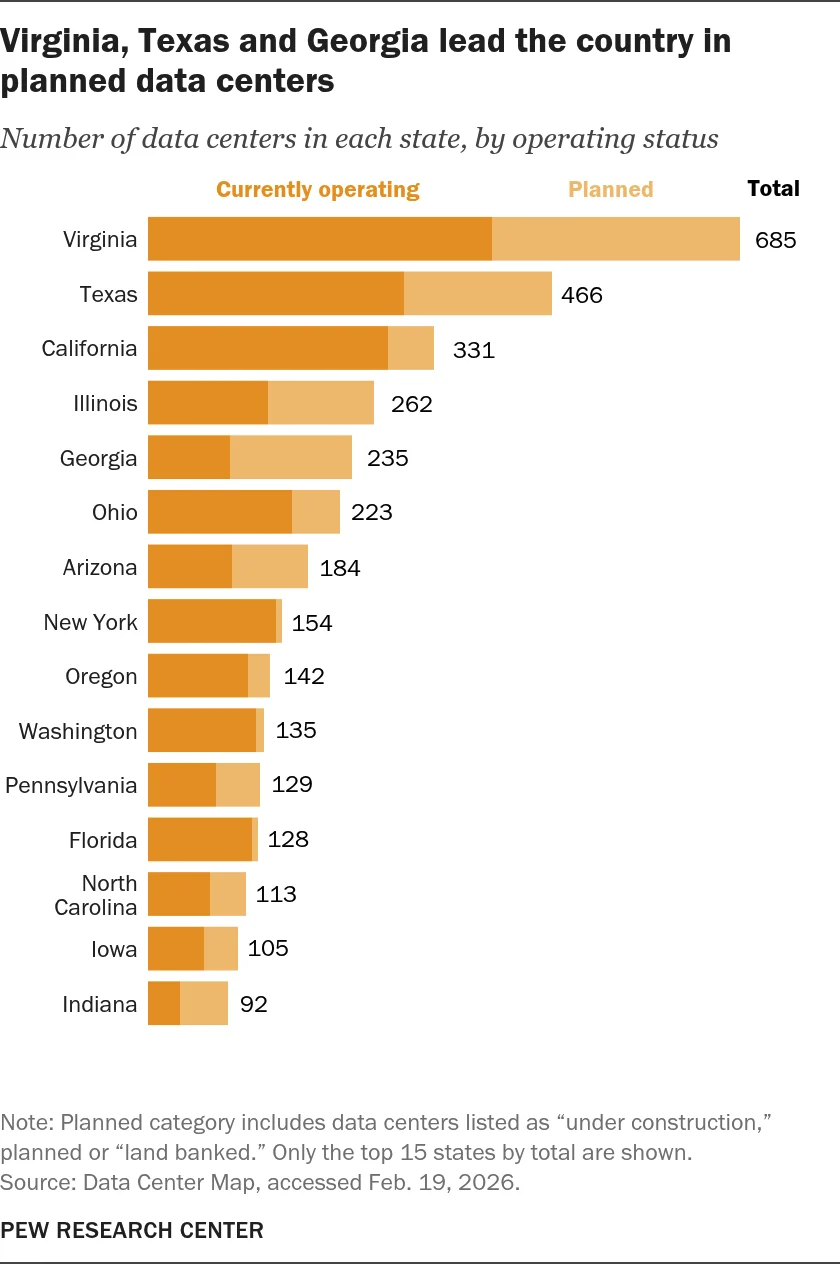

At the state level, Virginia and Texas stand out with the highest number of planned data centers, with 287 and 170 projects respectively. These states have historically been significant players in the data center market, and their continued growth indicates a sustained investment in digital infrastructure. Georgia follows with 141 planned centers, demonstrating its increasing prominence as a technology hub. Illinois (123) and Arizona (86) round out the top five states for projected data center growth.

Interestingly, the states leading in planned data center construction do not entirely mirror those with the most operational facilities. While Virginia (398) and Texas (296) also lead in existing data centers, California, a long-standing tech powerhouse, ranks third in operational centers (277) but has a significantly smaller pipeline of planned projects (54). This disparity might suggest a saturation of suitable sites in California or a strategic shift in investment towards regions with more growth potential and potentially lower operational costs. Ohio (166 operational, 57 planned) and New York (148 operational, 6 planned) also show a significant number of existing facilities, but with a more modest outlook for new construction compared to the leading states.

The Shadow of Data Centers: Proximity and Public Awareness

The increasing density and geographical spread of data centers raise questions about their proximity to American populations and the public’s awareness and perception of these facilities. The Pew Research Center’s survey data reveals that 38% of Americans currently live within a five-mile radius of at least one operational data center. This proximity is often amplified by the clustering of these facilities; nine out of ten data centers are located within five miles of another. Consequently, a significant portion of the population living near one data center is likely to be near multiple facilities.

Adding to this, an additional 4% of Americans live within five miles of a data center that is currently planned but not yet operational. When combined, these figures indicate that 42% of the U.S. population lives in close proximity to either an existing or a future data center. This growing proximity underscores the increasing tangible presence of the digital infrastructure in everyday American life, even if the facilities themselves are often discreet and their operations behind the scenes.

Despite this increasing proximity, the survey data suggests that living near a data center does not significantly correlate with higher public awareness of these facilities. Americans who reside near operational or planned data centers are about as likely to report having heard or read about them as those who live further away. Furthermore, there are no substantial differences in opinion regarding the impact of data centers on the environment, local energy costs, or job creation between those living near these facilities and those who do not. This suggests that while the physical footprint of data centers is expanding into more communities, the public’s understanding and engagement with their implications remain relatively uniform across different geographic locations.

Implications and Future Considerations

The ongoing expansion and geographical shift of data centers carry significant implications. Economically, the development of new facilities can bring substantial investment, job creation, and tax revenue to the communities that host them, particularly in rural areas that may be seeking economic diversification. However, this influx also brings challenges related to infrastructure demands, including power grid capacity, water usage, and transportation networks.

Environmentally, data centers are significant consumers of energy and water. The trend towards rural locations may offer opportunities for integrating renewable energy sources and implementing advanced cooling technologies to mitigate their environmental footprint. However, the sheer scale of growth necessitates careful planning and regulation to ensure sustainable development. The increased demand for electricity could also place additional strain on local power grids, potentially impacting energy prices and reliability for existing residents.

From a community perspective, the integration of large industrial facilities like data centers into rural landscapes requires transparent communication and engagement between developers, local governments, and residents. Understanding the potential impacts on local resources, land use, and community character will be crucial for fostering positive relationships and ensuring that the benefits of data center development are shared equitably. The Pew Research Center’s findings on public awareness suggest a need for greater educational outreach to inform communities about the role and impact of these critical infrastructure components.

As the United States continues to solidify its position as a global leader in digital innovation, the growth of its data center infrastructure will undoubtedly remain a key indicator of its technological trajectory. The evolving landscape, marked by a significant shift towards rural areas and a persistent, yet perhaps understated, public presence, demands ongoing scrutiny and informed discussion about the long-term implications for both the nation’s digital future and the communities that will increasingly host its unseen digital heart. The data compiled by Pew Research Center provides a critical foundation for understanding these trends and informing the policy and planning decisions that will shape the next chapter of America’s digital infrastructure.